What the New IRS Guidance on W2 Forms Means for Employers

Understand the IRS’s new 2025 rules for tips and overtime deductions and what employers need to update before 2026.

.png)

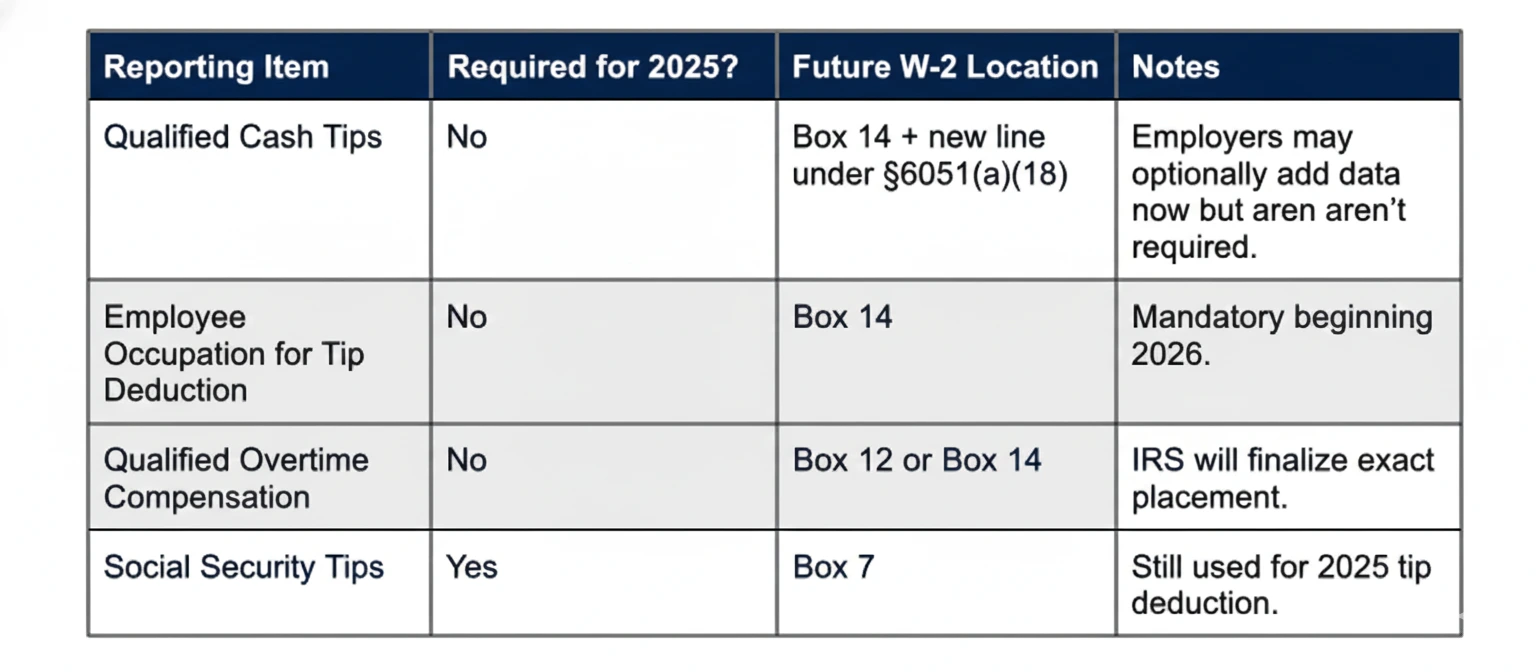

The Department of Treasury and Internal Revenue Services issued guidance for workers eligible to claim existing deductions for tips and for overtime compensation. Under the “One Big, Beautiful Bill,” millions of workers can deduct up to $25,000 in qualified tips and up to $12,500 in qualified overtime compensation on their personal tax returns for tax years 2025 through 2028.

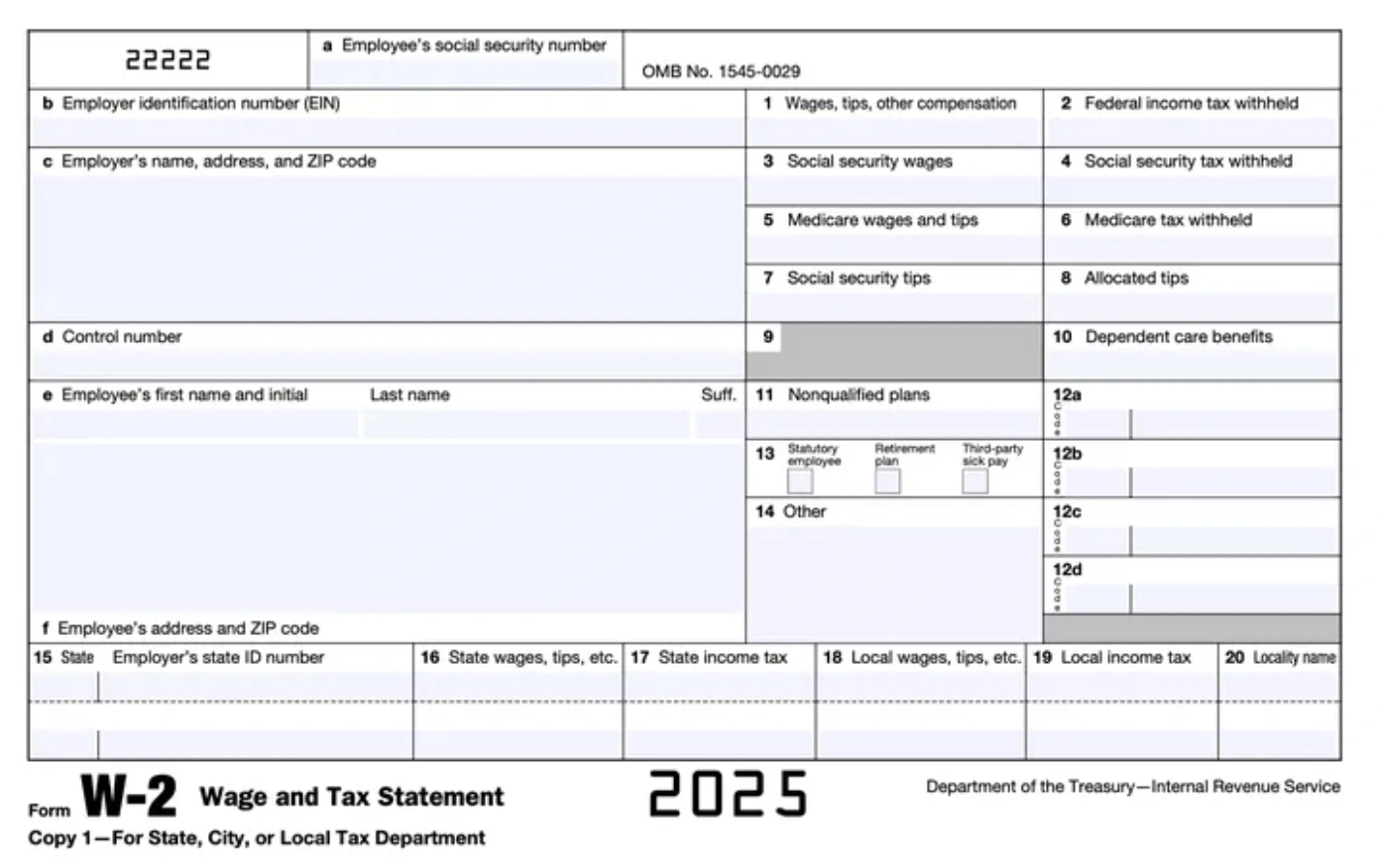

But here’s the catch: W-2s and 1099s are not changing for the 2025 tax year. That means payroll teams won’t report these amounts any differently, yet workers will still expect accurate information to claim the new deductions.

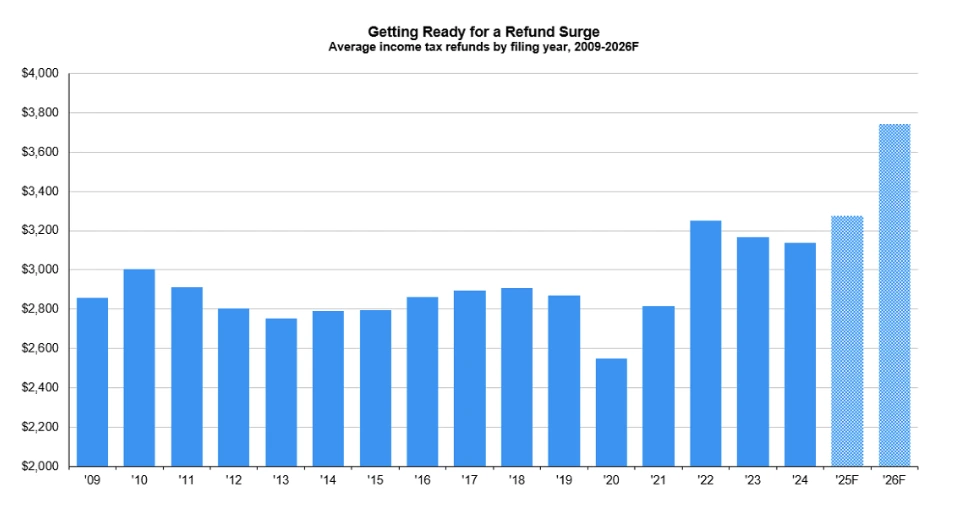

David Kelly, Chief Global Strategist at J.P. Morgan Asset Management, predicts higher income tax refunds early next year.

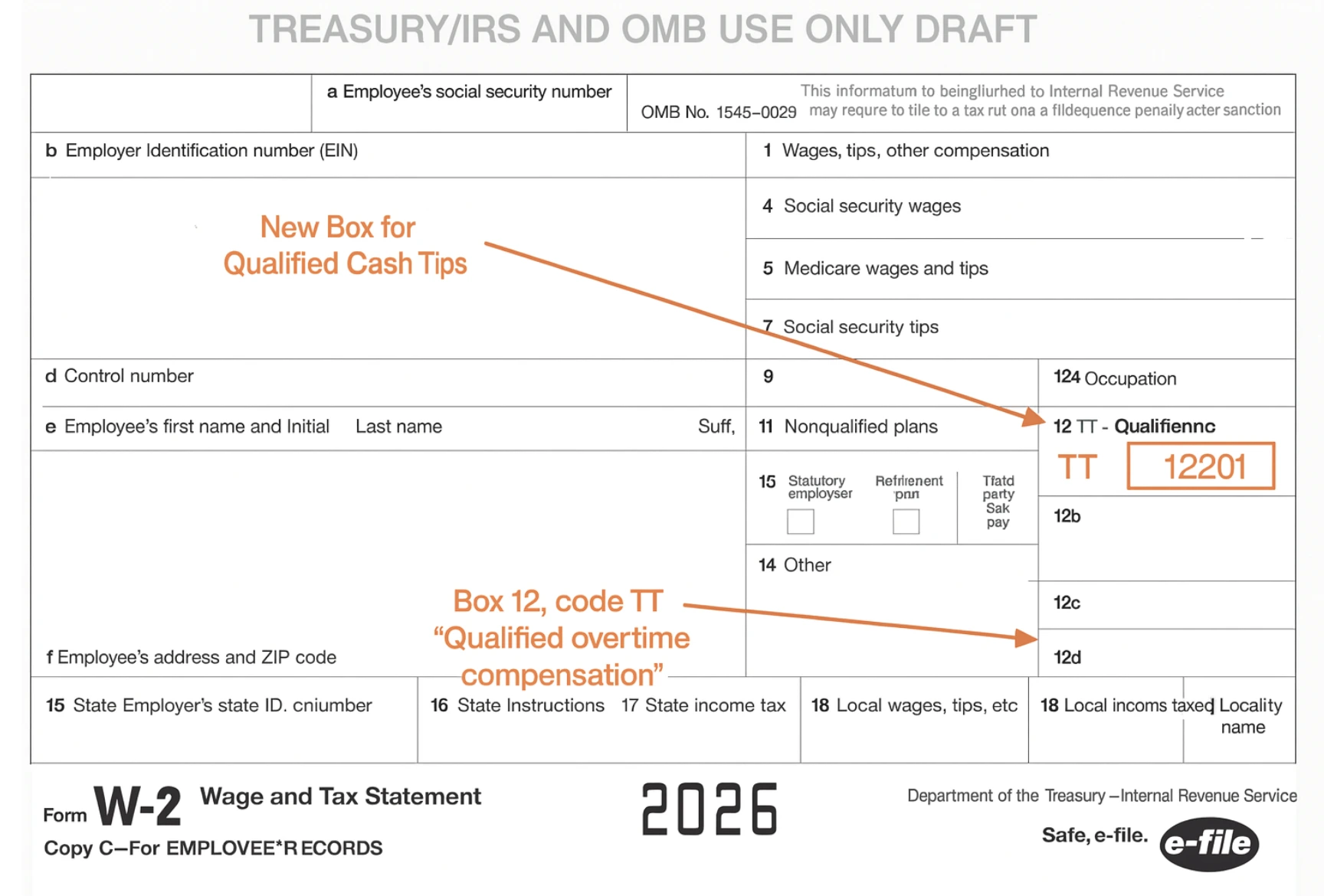

To bridge this gap, the IRS issued Notice 2025-69, offering transition relief for employers and providing detailed instructions for workers on how to calculate their deductions even without updated forms. Employers won’t be penalized in 2025 for incorrect or incomplete reporting, but that relief will expire by 2025 end.

For HR and payroll teams, this is not a minor update; it reshapes reporting workflows, employee communications, and compliance planning for 2026 across all frontline industries.

This blog breaks down precisely what the new IRS guidance means and how your organization should prepare for 2026.

What the IRS Just Announced (In Simple Terms)

Notice 2025-69 clarifies how workers can claim new deductions on qualified tips and overtime, even though employers are not required to change W-2 reporting yet.

Here are the three key points:

1. Workers can deduct qualified tips (up to $25,000/year).

This applies to cash tips, charged tips (including credit card tips), and any additional tips workers later declare on Form 4137. Tips received through third-party systems may qualify if workers maintain supporting records.

2. Workers can deduct the premium portion of overtime

Only the extra half-time required under FLSA (time-and-a-half) counts, and not the full overtime payment (up to $12,500 per return, or $25,000 for joint filers).

3. Employers receive transition relief for tax year 2025.

Employers are not required to change W-2, 1099-NEC, or 1099-MISC reporting. They will not be penalized for incomplete reporting related to qualified tips and overtime in 2025.

This relief gives employers time, but not forever. When final rules are issued, stricter reporting is expected.

Tip Deductions: What Employers Need to Know

The biggest confusion in 2025 will relate to how tipped employees determine the amount of qualified tips they can deduct.

According to the IRS, workers can use any of these sources:

- W-2 Box 7 (social security tips)

- Tips reported by employees to employers (e.g., Form 4070)

- Unreported tips added on Form 4137

- Daily tip logs (especially for self-employed workers or those receiving tips via TPSOs)

For employers, the W-2 Box 7 does not change, and they are not required to calculate or break out qualified tips. While not mandatory, the IRS notes that some employers may choose to provide additional information such as occupation details or internal tip summaries to help workers determine qualified tip amounts.

Key IRS examples (simplified)

Example 1: Restaurant server (Ann)

Ann is a restaurant server and their W-2 shows $18,000 in Social Security tips (Box 7). They didn’t report any additional tips separately using Form 4137.

What does this mean?

Ann can use the $18,000 shown on her W-2 as the total amount of qualified tips for their deduction. No extra calculation or additional forms are needed. If it’s on the W-2, they can claim a deduction.

Employer takeaway: For many employees, Box 7 alone will be sufficient. Workers may still ask you to confirm the number, but nothing additional is required on your side.

Example 2: Bartender (Bob): When Reported Tips Exceed the W-2

Bob reports $20,000 in tips to their employer during the year but their W-2 shows only $15,000 in Box 7 (tips subject to Social Security). They also have $4,000 of unreported tips that they will disclose on Form 4137.

What does this mean?

Bob can choose to share:

- The $15,000 mentioned on the W-2, with no additional evidence

- Or the $20,000 they reported to the employer during the year, with or without evidence

Either way, they can add the extra $4,000 of unreported tips. So their qualified tips could be:

- Option 1 = $15,000 + $4,000

- Option 2 = $20,000 + $4,000

Employer takeaway: Workers may ask why Box 7 shows a lower number than what they reported. This happens when some tips weren’t subject to Social Security tax. You’ll want your internal records (Forms 4070) organized to answer questions.

Example 3: Self-employed worker (Doug): When Workers Rely on Their Own Logs

Doug is a self-employed tour guide who earns $7,000 in tips, paid via a third-party payment system. Their 1099-K lumps all payments together and does not list tips separately.

What does this mean?

Because Doug kept documentation such as daily logs or other records to substantiate the tips, they can use the $7,000 as qualified tips even though the 1099-K doesn’t show it.

Employer takeaway: This matters to gig platforms, marketplaces, and businesses using contractors. Workers may ask how to verify tip amounts even if you don’t issue W-2s. Encouraging accurate worker logs can prevent confusion later.

Overtime Deductions: What Payroll Teams Must Prepare For

The overtime deduction applies only to the FLSA-required premium portion of overtime, generally the additional half-time above the regular rate, or the applicable premium under 29 USC § 207.

- Workers deduct only the FLSA-required premium portion, not total overtime pay.

- If payroll doesn’t break it out, workers will calculate it using IRS formulas.

- Employers need clean overtime classifications before 2026, when penalty relief ends.

Employees exempt from Fair Labor Standards Act overtime rules (salaried exempt under white-collar exemptions, certain professionals) cannot claim the deduction.

Example 4: Law enforcement employee using the FLSA “work period” rules

Maria works in law enforcement and is treated as a nonexempt employee under the FLSA. Their agency follows the special 14-day “work period” schedule, allowed under FLSA section 7(k). During 2025, they earn a total of $15,000 in overtime pay under this work-period system.

To figure out what portion of this qualifies for the new deduction, Maria uses the IRS method for law enforcement and fire protection roles: divide total overtime pay by three. So their qualified overtime compensation for 2025 is:

$15,000 ÷ 3 = $5,000

This amount, not the full $15,000, counts toward their annual limit for the deduction against overtime premium.

Employer takeaway:

Organizations using Section 7(k) work periods (such as police, fire, and certain public safety roles) should review their FLSA classifications and overtime calculations now. These roles follow different overtime formulas than standard 40-hour employees, and workers may ask payroll to confirm how their qualified overtime number is derived.

Summary Box

Risks of Doing Nothing in 2025

While the IRS has offered transition relief for 2025, adopting a wait-and-see approach is still risky for employers. The most immediate risk is rising employee frustration. Tipped, hourly, gig, and frontline workers will depend heavily on their employers to help them understand how to claim these new deductions, and a lack of clear information will quickly turn into higher support volume and dissatisfaction.

Payroll errors also pose a serious threat. Any inaccuracies in how tips or overtime premiums are captured today may seem harmless under the temporary relief. However, those errors will compound when full penalties resume in 2026, leading to employee filing issues, compliance exposure, and strained employee relations.

FLSA misclassification adds another layer of risk. If overtime codes or exempt/nonexempt classifications are incorrect now, the downstream tax implications can multiply, making corrections later far more costly.

Final Thoughts

Employers who fail to offer clarity may be viewed as unsupportive or unprepared. At the same time, those who take proactive steps now will strengthen trust, improve retention, and position themselves as employers of choice in a highly competitive labor market.

If you want to streamline compliance before the 2026 rules tighten, now is the time to evaluate the right tools. Book a demo with Firstwork and see how automated workforce activation, verification, and compliance management can keep your teams prepared for what’s coming next.